What Leaders Need to Understand to Design A Resilient Recovery

In this video, Aspen Institute Director of Insights and Evidence Gen Melford has broken down the Aspen Institute Financial Security Program’s new financial security framework – in less than ten minutes. Watch here or read the explanation below.

What We Think of When We Say “Financial Security”

In our work we have adopted the Consumer Financial Protection Bureau’s consumer-driven definition of financial well-being as our north star, so we use the terms “financial security” and “financial well-being” interchangeably.

In a nutshell, financial security means having enough money and resources to comfortably meet your needs and obligations, protect you from shocks, pursue your goals, and enjoy life – both in the present and the future.

We think of financial security as an outcome goal – a state of being that exists when the key components are in place.

What it Takes to Have Financial Security — Really

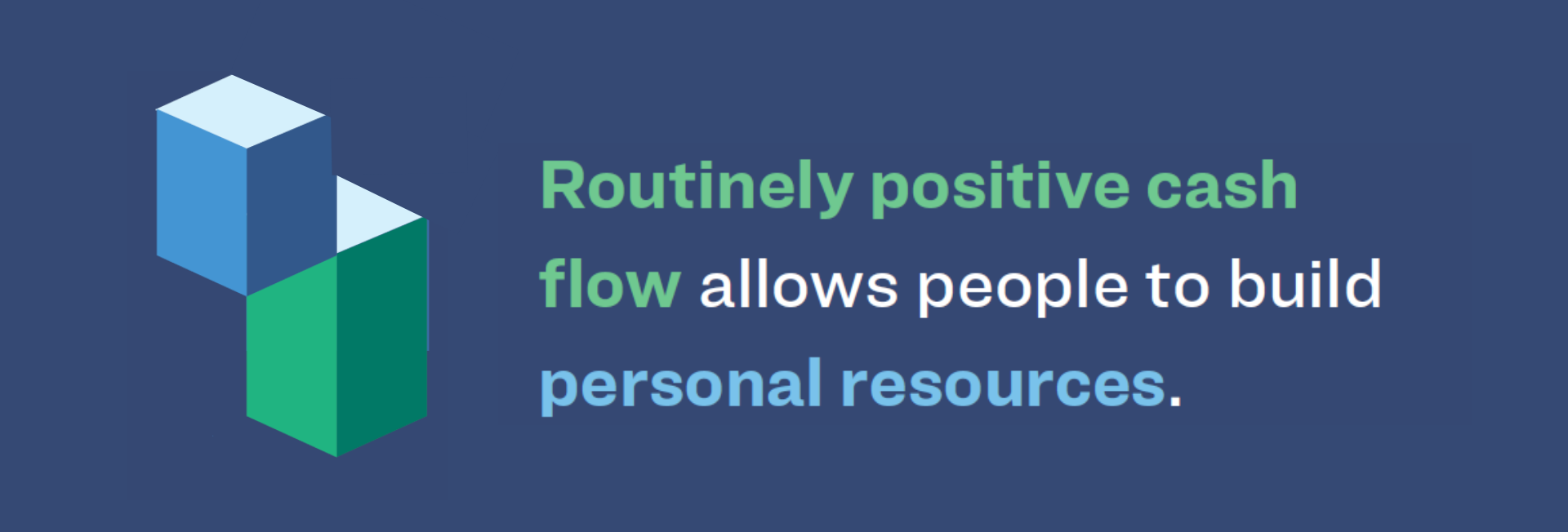

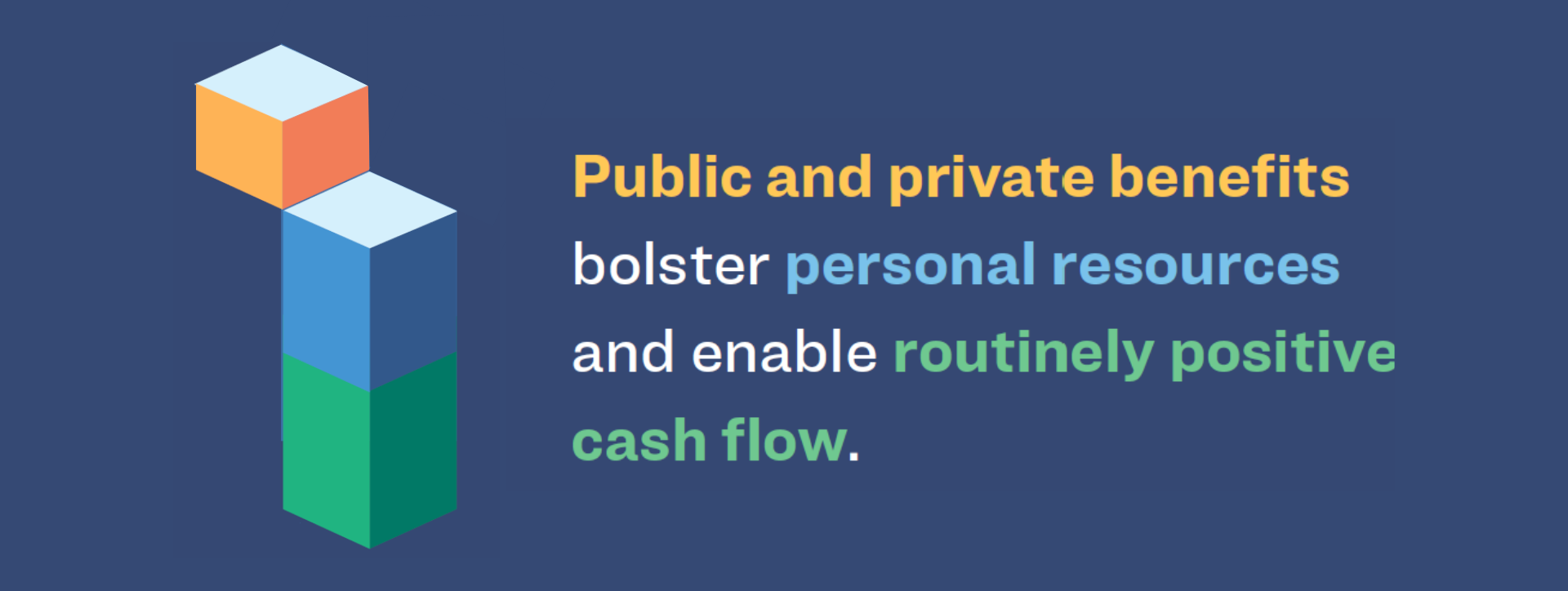

But thinking about financial well-being as simply the amount of money people have on hand at a given moment is deceptive, and when we fail to dig deeper, we risk creating poor policy. At its most basic level, there are three pillars of financial security: routinely positive cash flow (income that typically exceeds core expenses); personal resources (savings and financial cushions); and public and private benefits.

While savings are a key indicator and source of financial security, in taking a snapshot only of a household’s personal resources at a point in time, we miss two interconnected pillars that enable households to achieve – or fail to achieve – financial security. Namely: the ways money comes into a household (labor income and non-labor income), and all the ways it goes out (debt payments and expenses); and benefits. In actuality, financial security rests on three interconnected pillars.

The First Pillar: Routinely Positive Cash Flow

Routinely positive cash flow is the foundation of people’s financial life. Quite simply, this means income minus expenses, and this forms the basis of how households experience their financial situation. Gaining employment, a raise or promotion, or simply more predictable and less volatile income are key factors found to increase financial health and well-being. On the other hand, losing a job or having hours reduced or facing a major medical or other expense are key predictors of declining financial health and well-being. When people reliably have more income – from any source or combination of sources – than the cost of meeting their basic needs, then they can pay their bills and still have extra money to put into savings.

The Second Pillar: Personal Resources

Having personal financial resources boosts financial security; a lack of them pushes people into instability. Not only do readily accessible savings protect against material hardship, they also provide the material resources and mental bandwidth for people to be able to weather smaller financial shocks without getting knocked off track from working toward their longer-term goals. Personal resources provide the opportunities to invest in family well-being, asset building, and economic mobility.

Liquid savings are a particularly valuable barometer of financial security. Early research by the CFPB found that liquid savings is the single variable most highly correlated with financial well-being. More so even than income. This makes intuitive sense, as savings can be seen as both an outcome of having routinely positive cash flow, and a key form of financial stability in its own right. Several recent studies confirm that having higher levels of liquid savings does protect against declines in financial health and well-being in the face of relatively limited expense shocks.

The Third Pillar: Public and Private Benefits

People cannot fully insure themselves all the time. Whether or not we realize it, everybody relies on safety nets or social insurance. Research shows that while liquid savings and other personal resources are incredibly valuable, they can’t protect people against larger or more persistent shocks, such as job loss or major medical expenses. One recent study found that even the most financially responsible people are no more protected against loss of financial security in the face of major financial shocks than everyone else.

COVID-19 is but the latest example of major, economic shocks that households will never be able to fully weather on their own. This spring over 30 million people found themselves suddenly out of work – and while the “rule of thumb” is to have 3 to 6 months of personal savings to protect one’s self, the reality is economic downturns are lasting longer than that.

Yet it is not just the public sector providing insurance against shock – the private sector does it too. The question, then, around benefits shouldn’t be: Do people need social insurance? It should be: “How do we work together to design and deliver a system of benefits – public and private – that is fair, equitable, efficient and effective?

How Money Moves through a Household

We must consider the relationship between the three pillars if we are to understand how household finances works. The graphic below shows how the three pillars work together to enable families to achieve – or fail to achieve – financial security.

1. Routinely positive cash flow is the foundation. When people reliably have more income (including labor and non-labor income) than the cost of meeting their basic needs, they can pay their bills and still have extra money to put into savings.

2. Personal financial resources (financial cushions and wealth) are critical for maintaining stability in the face of smaller income or expense shocks and provide the resources that people can invest in family well-being, asset building, and economic mobility.

When cash flow is reliably positive, people can build savings and wealth and can use those resources to invest in various ways to produce more income or to reduce their ongoing expenses, thereby increasing cash flow, choice and security, in a virtuous cycle.

But when income does not reliably cover core cost of living expenses and allow for saving, the consequences are often unmanageable debt, late fees, and other expenses that further weaken cash flows, in a vicious cycle of financial stress and instability.

3. A wide range of public, employer, and third-party benefits – we give a number of examples of these in our report – can provide households with income, reduce cost of living expenses, and support household wealth-building and economic mobility. In doing so, benefits strengthen the other two pillars and protect households from risks too big to self-insure against. A lack of benefits providing insurance can deprive families of consistent cash flow and siphon their wealth and security, resulting in spirals of debt or poverty.

How Leaders Can Use This Framework to Boost Financial Security for All

With this framework in hand to diagnose and pinpoint exactly which components of financial security are missing for households, leaders in all sectors can boost access to different aspects of the pillars.

They can boost labor income, benefit income, or capital income. They can reduce various cost of living expenses. They can help people capture net income and turn it into savings. They can invest in household balance sheets and help households reduce burdensome debt. And they can provide group and social insurance to protect households in the face of life’s big shocks.

Making these ideas real will look different for different leaders – depending on the levers over which they have influence and the specific needs of the households they serve – and will likely require different ways of working together, with a laser focus on strengthening the systems that can boost household cash flows and balance sheets and protect households from the big risks outside their control.

To Read More

For More Information, including research and data on each pillar, download “The State of Financial Security 2020: A Framework for Recovery and Resilience.”

To read more about Aspen Institute’s Benefits21 initiative, which focuses on creating and implementing an integrated, modernized system of benefits that ensures financial security and economic dignity for all workers click here.