I. Thinking Long Term

Once called “the most influential financial institution in the world,” BlackRock, Inc. can cause a hush in the corner offices of the corporations where they invest. “Corporations where they invest” is quite a broad category; BlackRock is the single largest shareholder in one of every five U.S. corporations, including ExxonMobil, IBM, and Verizon, and they own at least five percent of the stock in 1,800 of the 4,300 companies on the NYSE and NASDAQ exchanges. So this spring, when BlackRock CEO Larry Fink released a letter expressing ‘concerns’ about short-term thinking in capital markets, people noticed.

Fink outlined the responsibility of BlackRock and others in the capital markets to challenge the trend of short-termism, and highlighted why long-term thinking is so important. Speaking rather directly, he called it, “investing in the future growth of their companies.”

Plainly put, Fink wrote:

Corporate leaders can play their part by persuasively communicating their company’s long-term strategy for growth. They must set the stage to attract the patient capital they seek: explaining to investors what drives real value, how and when far-sighted investments will deliver returns, and, perhaps most importantly, what metrics shareholders should use to assess their management team’s success over time.

Analysts and researchers at the Aspen Institute Business and Society Program heard a familiar refrain. They have spent years probing the causes behind and sounding the alarm about short-termism at U.S.-listed corporations, publishing numerous papers and articles on the subject. They have also convened a coalition of business leaders, investors, corporate governance experts, labor leaders, and academics to discuss the coming challenges posed by short-term thinking, and to investigate possible ways to hardwire more sustainable strategies into the boardrooms and trading floors.

In 2007, that unique coalition, known as the Aspen Institute Corporate Values Strategy Group (CVSG), produced the Aspen Principles for Long-Term Value Creation which offered a framework for both corporations and investors to focus on long-term value rather than short-term movements in stock price. In the wake of the 2008 financial crisis, Aspen CVSG released a follow- up to “the Aspen Principles” outlining policy recommendations for overcoming short-termism. The policy recommendations were signed by prominent individuals from business, finance, and policy like Warren Buffett, John Whitehead, Martin Lipton and Lou Gerstner.

These principles aren’t the work of spoilsports hoping to somehow de-fang the marketplace. Rather, the aim of the CVSG is to inject stability and sustainability into the capital markets. In turn, these more stable markets would set the stage for stronger corporations, a better economy and maybe fewer big financial disasters roiling the globe. The accounting scandals at Enron, WorldCom and Nortel in the early 2000s are object lessons in how unrealistically high expectations from the stock market and analysts can lock in short-term thinking and behavior. The surge in the use of stock options as executive compensation further aggravated the problem, combining with analyst expectations to create an unmanageable conflict between the demand for ever-rising profits and a long-term strategy for thoughtful growth.

While Wall Street sometimes specializes in short memories of bad news, those scandals should remind us that short-termism and an outsized focus on meeting outsider expectations — rather than building real value — is a recipe for unstable growth and devastating destruction of value.

II. The Role of Corporation

After the 2008 financial crisis, the most overt examples of short-termism may have gone to ground for a while. New regulation chastened the worst actors, and the lending sector found a way to rebuild its sky-high profits without the same laxity that contributed to the meltdown. The Aspen Institute team kept a close eye on the short-term thinking they saw as a pernicious force lurking in the darker corners of Wall Street and boardrooms. Their advocacy to root out this counterproductive practice led to some compelling findings about the pace of change in corporate America. Changing minds, in some cases, came easier than changing the systems that govern corporate America and the financial industry.

The Corporate Values Strategy Group began to examine links between the epidemic of short-term thinking and bigger questions about the purpose of the corporation starting in 2011. Could the idea of the corporation be reimagined to reflect a better, more sustainable approach? Is the purpose of the corporation to enrich its officers, create value (or, differently, create profit) for its shareholders, or make happy customers? Do different responsibilities (to improve the world, or at least not do the opposite) impact these? The questions, and the Strategy Group’s larger work on corporate purpose, come back to how we will, in the present and long into the future, evaluate the success of business leadership. Will we remember the kind of leadership that can be summed up solely on a balance sheet? Or do we owe future generations a vision of business leadership that leads to a better, more stable system?

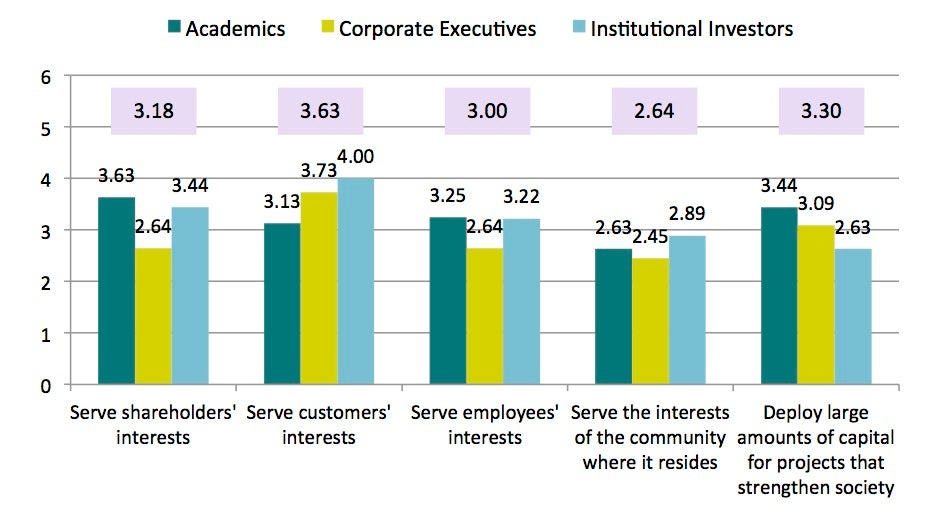

To address these fundamental questions, researchers commissioned by the CVSG tried to dig below the surface and find some common understandings about the purpose of the corporation. They conducted in-depth interviews earlier this year with people at different points in the ecosystem around Wall Street: investors, corporate executives, and academics, to name a few. To the surprise of no-one, they revealed a broad diversity of opinions on the question of the primary purpose of a corporation. The responses at times resembled a graduate class on good and evil in the philosophy of Adam Smith. The entire report, Unpacking Corporate Purpose (PDF), provides an eye-opening view into what is truly the battle for the soul of the corporation.

Close to the action of this ongoing debate between managing directors and tenured professors was a second, more nuanced conversation that linked the question of corporate purpose and the concerns about short-termism. When respondents asserted that the purpose of a corporation is to create ‘value’ for the shareholder, did they mean Larry Fink’s “long-term strategy for growth” and “far-sighted investments” or were they merely talking about squeezing out the right earnings report to meet analyst expectations? Who got to pick what we mean by “value” and what we mean by “profit?”

The answer might surprise you. Even participants in the Unpacking Corporate Purpose study who firmly believe in the power of the market to ultimately determine the right outcome struggled to link the quarterly race for more profits with any notion of value creation. Indeed, for different actors, often when it was easy to do so and even sometimes when it wasn’t, they gradually explored the space between turning out short term gains and creating lasting value for the shareholder.

Some of the responses were revealing. Various people — holding different roles across academia, as well as institutional investors and private fund managers — express a preference for real value creation over quick profit-taking — an evident vote for long-term thinking and acting.

A vice president at a large fund management firm (the participants in the report all agreed to be identified but their quotes are not for attribution) noted the tension between short- and long-term results:

Because a lot of us say we’re long-term investors, but if companies don’t meet those very short-term goals and have results quarter after quarter, often we as institutions do things that completely negate our focus on the long-term. And I think that’s where the struggle is. It’s really short-term vs. long-term.

A managing director at another investment fund moved further down that rhetorical road, zeroing in on the challenge of taking the long view:

I don’t care about a stock price minute to minute, because over a long time horizon, the markets are efficient and the stock price will reflect the value being created in a company. That value is best created when you make good decisions that treat your employees well, treat your customers well. I think they’re completely intertwined in the long term. And again, the problem of having a Bloomberg terminal on your desk and looking minute to minute is one that management has to fight very hard.

Another managing director talked about the natural tension between management and investors (in the form of a board of directors) when focusing on products customers actually want.

The board will say, these product plans you have, we don’t have the money for that. We need to be throwing off dividends or we need to be goosing earnings in the next quarter. And then management says, if we don’t invest in these products, we won’t have something to sell a few years from now. …I think the board will often put pressure on earnings, and management will have to push back if they don’t have a way to goose earnings in the short run, and the way the board is suggesting would hurt the prospects for the long run in terms of continuing to have products that are valued by the clients.

Following this thread through the research — weaving around deeply divided beliefs about the purpose of the corporation — is fascinating. At times, corporate officers themselves feel helpless to fight the power of short-term thinking, to resist the gravitational pull of profit-reporting. One executive in the study put it this way:

To me, when I look at a quarter’s result… I’m asking myself, what does this tell me about the plan we have for the year? Is it the right path or not? Do we have to make some adjustments or not? I’m not near as concerned about whether I hit a particular number. But when you have analysts who go nuts over a specific number and if you miss it by a penny, the market goes crazy, that’s a weird reaction that isn’t justified by the facts.

Conclusion: The Invisible Hand vs. the Squeaky Wheel

The powerful pull of quarterly earnings reports doesn’t happen in a vacuum. The “analysts” referred to above by the executive from the study may hint at a small reform which could yield big benefits. The business press talks about activist investors’ or even hedge fund investors as loud voices driving short-term thinking . But a particularly large helping of the scorn or praise that follows earnings reports comes from investment bank analysts — “sell-side” analysts — who are paid a premium for delivering exclusive information and driving market moves. Critics charge that sell-side analysts are compensated for increasing stock trading volume, and are inclined to generate buzz that inspires more trading, not holding. The sell-side’s power in shaping the expectations of the markets can often skew the importance of quarterly earnings reports and amplify short-term information about companies which often has little relation to a company’s long-term prospects.

In a sense, these outsized voices are a ‘squeaky wheel’ — and some might say a distraction — to the more deliberate movement of Adam Smith’s ‘invisible hand.’ Because they enjoy a front row seat at quarterly profit conference calls and a hotline to the business press, they can sometimes crowd out more important questions about the long-term planning and health of a corporation.

So what are the next steps? How do researchers and practitioners take direction from this range of findings? These issues represent a kind of identity crisis for people who think about and practice business today: How do we manage the dangers presented by short-term thinking to the sustainability of the financial system for America (and the wider world)? And is the purpose of a corporation merely to serve as a money-making entity, or do corporations have a responsibility to represent true leadership in the business sector for generations to come?

Acknowledging that the landscape has radically changed is critical to understanding where this conversation goes next. Four years after the Dodd-Frank Wall Street Reform and Consumer Protection Act became law, there have been some important changes focused on accountability and a rebalancing of interests. But we have also seen bank profits soar even as they take on fines and other penalties for bad acts during the 2008 financial crisis. We may well be at a fork in the road: In one direction, we can repeat the mistakes of the past, continuing to chase quarterly profit goals and squeeze more profit from less strategic investment; in the other, we can realize a broader definition of the purpose of the corporation as a thriving, functional part of larger society, serving shareholders, customers, employees and the greater good.